What is Hazard Insurance and Why Do I Need it for My Home?

The Critical Role of Hazard Insurance in Homeownership

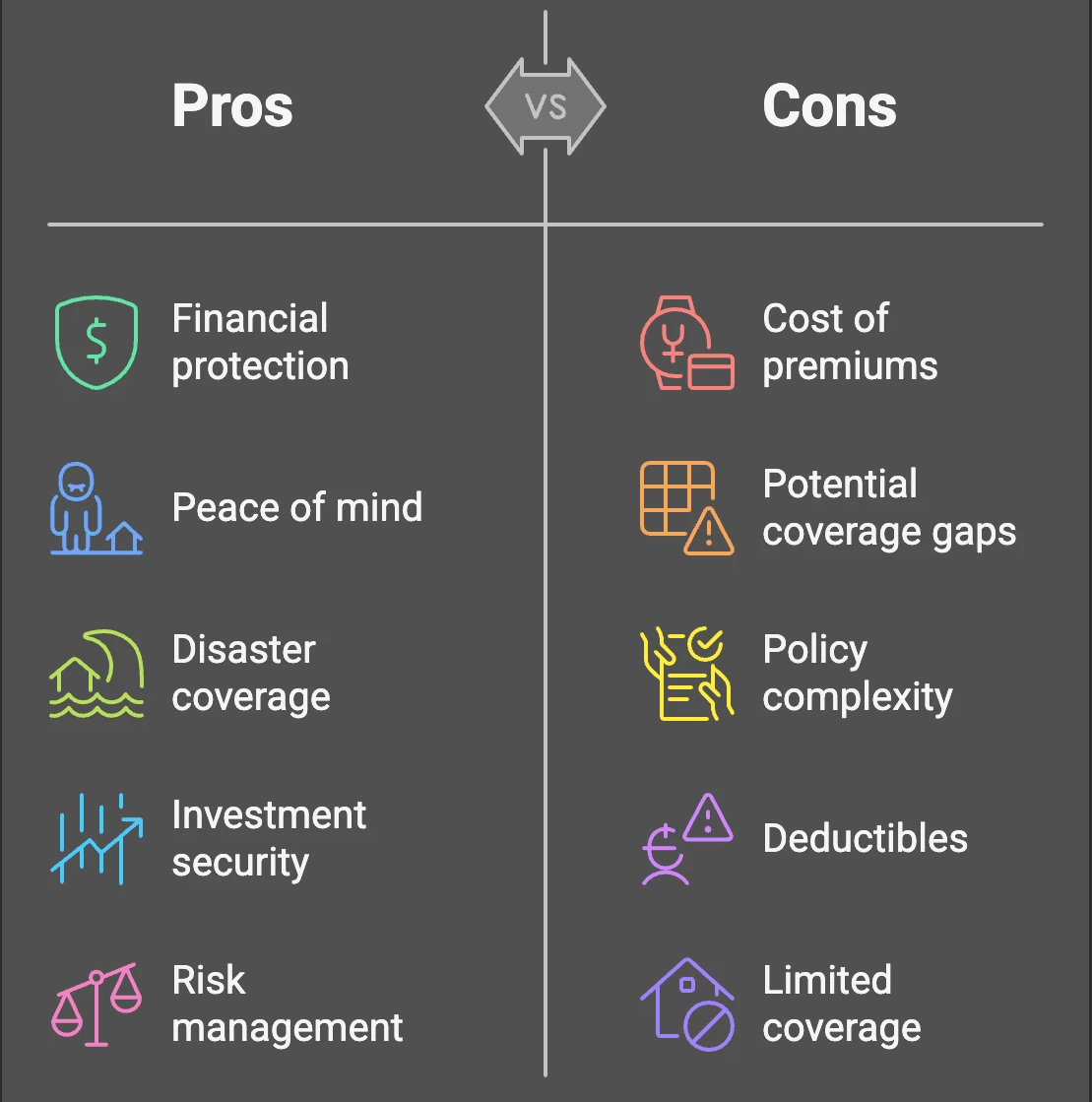

Buying a home is one of life’s biggest investments, so protecting it is a must. This coverage acts as a powerful safety net, shielding your property from unexpected disasters that could otherwise bring overwhelming financial loss.

Hazard Insurance: Coverage that protects property owners against physical damage or loss caused by specific perils like fire, storms, vandalism, and other natural disasters. This type of insurance is typically required by mortgage lenders and is usually included as part of a standard homeowner's insurance policy.

Understanding Hazard Insurance Coverage

Your hazard insurance policy shields your property from various threats. Here's what you can expect to see covered:

Fire and smoke damage: Including both the direct flames and resulting smoke damage

Wind and hail damage: From minor roof damage to major structural issues

Lightning strikes: Both direct hits and resulting electrical surges

Falling objects: Such as tree branches or debris

Vandalism and theft: Protection against human-caused damage

However, standard hazard insurance won't cover everything. These items typically need separate policies:

Flood damage

Earthquake damage

Normal wear and tear

Pest infestations

Hazard Insurance vs. Homeowner's Insurance

Many people mix up these two types of coverage. Think of hazard insurance as a subset of homeowner's insurance. While hazard insurance focuses on property damage from specific events, homeowner's insurance includes liability coverage, personal property protection, and living expenses if you're displaced.

Cost Factors and Considerations

Your premium depends on several factors:

Where your house sits (flood zones, fire risk areas)

The current market value of your property

How much coverage you select

Your chosen deductible amount

Which insurance company you pick

Requirements and Regulations

Most mortgage lenders require hazard insurance - they want to protect their investment too. Each state sets its own rules about minimum coverage requirements. Make sure you keep your policy documentation handy, as your lender might ask to see proof of coverage annually.

Making a Hazard Insurance Claim

If disaster strikes, follow these steps:

Document all damage with photos and videos

Contact your insurance company immediately

Keep receipts for any emergency repairs

Work with your assigned claims adjuster

Common Questions and Misconceptions

Q: Do I need hazard insurance if I don't have a mortgage?

While not required without a mortgage, protecting your investment still makes sense.Q: What happens if my coverage lapses?

Your lender might buy force-placed insurance at a much higher cost to you.Q: How much coverage should I get?

At minimum, enough to rebuild your home at current construction prices.

Tips for Choosing the Right Coverage

Take time to evaluate your property's specific needs. Compare multiple policies and insurance providers. Review your coverage annually - construction costs and property values change over time.

The Future of Hazard Insurance

Insurance companies now use sophisticated data analysis to assess risk. New technology helps predict weather patterns and potential hazards. Some companies offer smart home discounts for installing monitoring systems.

Don't wait until disaster strikes to think about hazard insurance. Bellhaven Real Estate offers free consultations to help you understand your insurance needs during the home buying process. Our team knows local requirements and can guide you toward appropriate coverage levels for your property.