Last Updated in March 2025

Earning $50,000 per year puts homeownership within reach in most areas of the US, but exactly how much house? I'll break down the math using common lending formulas and current market conditions to give you a realistic target.

Quick Answer: With a $50k annual income you can afford a home between $156,100 and $239,700. Honestly though… your home buying power depends on way more than just your salary. Your credit score, current debts, down payment, and even where you want to live all play huge roles in what you can actually afford.

↓ Find out exactly how much you can afford below ↓

Factors affecting affordability

To simplify calculations, we'll use a middle ground on a home purchase price of $195,100. For exact figures on your specific scenario, be sure to use our calculator above.

Interest Rates

Rates aren't what they were in 2021. As of March 2025, mortgage rates are hovering around 6.7%.

Every 1% change in interest rates can increase or decrease your buying power by roughly 10%. So if you could afford a $195,100 home with the current rate at 6.7% you might only qualify for $175,600 if the rate jumped to 7.7%. If rates dropped down to 5.7% you could qualify for $214,600.

Down Payments

You don't necessarily need 20% down anymore. Options range from nothing down with USDA loans to the traditional 20% down payment that eliminates mortgage insurance.

For a $195,100 home on your $50,000 salary:

3.5% down = $6,829 (minimum for FHA)

10% down = $19,510 (common middle ground)

20% down = $39,020 (eliminates PMI)

The smaller your down payment, the higher your monthly costs - but waiting years to save 20% means potentially missing out on building equity and market appreciation.

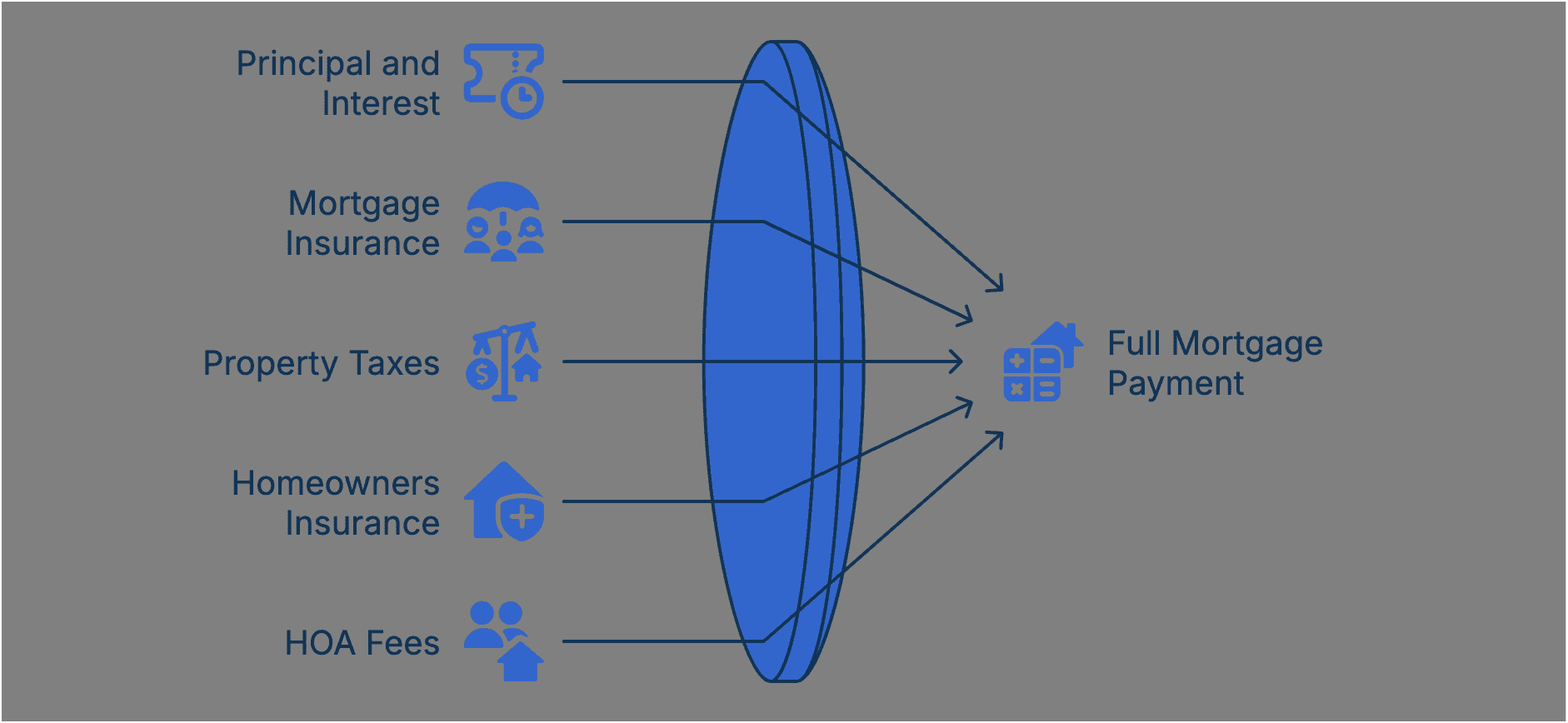

Monthly Homeownership Costs

Your mortgage payment is just the beginning. Don't forget, on a $195,100 house you'll have:

Property taxes: $131 monthly depending on location

Homeowners insurance: $88/month depending on many factors

Possible HOA fees: Can range from $50 to $500+ monthly

Maintenance: To be on the safe side, budget about 1% of home value annually (that's $1,951 yearly on a $195,100 home)

Credit Score

With a credit score above 740, you'll snag the absolute best interest rates out there. Drop below 700, and you'll start paying more every single month for the exact same house.

How much more? On a $195,100 home, the difference between 'excellent' and 'fair' credit could cost you an extra $62+ per month. That's $22,320 over a 30-year loan!

Debt-to-Income Ratio

Let's talk about the number that actually determines your home-buying power... your Debt-to-Income ratio (DTI).

Most lenders look at your total monthly debt compared to your income. They generally aim to keep it around 43%, but a lot of programs will stretch to 50% or even higher for qualified borrowers!

Here is what the math would look like if you had $400 in current monthly debts.

Convert your annual salary into monthly salary ($50,000/year = $4,167/month)

Multiply your monthly salary by the desired DTI ratio ($4,167 x 43% = $1,792)

Subtract your monthly debt payments ($1,792 - $400 = $1,392)

The $1,392 is what you'd have available for a maximum mortgage payment

In todays market, with 5% down, a $1,392 mortgage payment would let you buy a $186,200 house.

Rules of Thumb for buying a house on a $50k income

There are two common 'rules of thumb' thrown around. 'The rule of 3' and 'The 28/36 rule'. Honestly, both of them are super crude, but in a pinch can get the job done. You're better off scrolling to the top of this page and using our calculator to really find out what you can afford.

The Rule of 3 for someone with a $50k salary

The Rule of 3 suggests you can afford a home that's roughly 3 times your annual income. So if you're making $50,000 a year, this rule would put your max home price around $150,000.

Think of it as a quick check before you dive into all the complicated calculators and debt ratios. If someone making $50k is looking at a $450,000 house, this rule immediately signals 'Hey, that might be stretching things WAY too far.'

The Rule of 3 naturally builds in a buffer for all those other life expenses you've got going on. Because honestly… you're not just paying for a house! You've got retirement to save for, maybe some travel plans, and just living in general.

The 28/36 Rule for someone with a $50k salary

The 28/36 rule suggests you shouldn't spend more than 28% of your gross monthly income on housing costs and no more than 36% on total debt payments.

Let's break this down for your $50k annual income:

Your monthly income before taxes is about $4,167. So:

Housing costs should ideally stay under $1,167 per month (that's 28%)

Your total monthly debt payments (including your mortgage, car loans, student loans, credit cards - the whole shebang) shouldn't exceed $1,500 (that's 36%)

But wait - what counts as 'housing costs'? It's not just your mortgage payment! We're talking:

I've seen so many first-time buyers focus only on the mortgage payment and then get totally blindsided by these other costs. Trust me, they add up fast!

Now, are these rules set in stone? Nope! It's more of a starting point. Most lenders will let you stretch far beyond these numbers. And honestly, in high-cost areas, many people end up spending more than the rules show anyway.

Affordability Scenarios

Alright, let's get into the nitty-gritty with some real scenarios based on your $50k income. I'm going to break down three different approaches so you can see what feels right for your situation.

Conservative Approach

If you're the type who likes to sleep soundly at night knowing your finances are rock-solid, this approach is for you.

Recommended home price: Around $156,100

Down payment: 5% ($7,800)

Monthly payment breakdown: | |

Mortgage (principal + interest): | $957 |

Mortgage Insurance: | $35 |

Property taxes: | $105 |

Insurance: | $70 |

Total monthly housing cost: | $1,167 |

This approach means you'll have a cushier monthly budget, and still have money left for other life goals like retirement, travel, or that vintage motorcycle collection you've been eyeing.

The trade-off? You might get less house than your friends who are stretching their budgets. But hey, you also won't be eating instant noodles for dinner when unexpected expenses pop up!

Balanced Approach

Most of my clients end up somewhere in this middle ground - getting a nice home without sacrificing their financial future.

Recommended home price: Around $195,100

Down payment: 5% ($9,800)

Monthly payment breakdown: | |

Mortgage (principal + interest): | $1,196 |

PMI: | $44 |

Property taxes: | $131 |

Insurance: | $88 |

Total monthly housing cost: | $1,458 |

With this approach, you'll still have plenty of funds to enjoy your life and put a little bit of money away. The trade-off? You'll start budgeting regularly to stay on top of things, every dollar should be planned out.

Maximum Buying Power

Look, sometimes you just want the nicest house you can possibly get. If you're comfortable devoting more of your budget to housing and don't mind a bit more financial risk, this option shows what's possible.

Recommended home price: Around $239,700

Down payment: 5% ($12,000)

Monthly payment breakdown: | |

Mortgage (principal + interest): | $1,469 |

PMI: | $54 |

Property taxes: | $161 |

Insurance: | $108 |

Total monthly housing cost: | $1,792 |

Fair warning: This approach leaves less wiggle room in your budget and might make other financial goals tougher to reach. But if housing is your top priority and you're confident your income will grow over time, it can make sense.

Many of my clients start with something closer to this approach for their first home, then shift to a more conservative strategy as their family and financial needs evolve.

Remember, there's no 'perfect' scenario that works for everyone making $50k - it all depends on your unique situation, future plans, and how much house matters to you compared to other things in life!

Qualification vs. Comfort

What the bank says you can afford and what actually feels comfortable in your real life are often two completely different numbers!

I've seen it countless times... lenders approve someone making $50k for a mortgage that would leave them eating ramen and skipping vacations for the next 30 years…

The Qualification Number: Based purely on your income, debt ratio, and credit score, lenders might approve you for a loan up to 50% of your pre-tax income. On your $50k salary, that could translate to a mortgage as high as $275,700... or even higher!

But wait - just because you can doesn't mean you should!

The Comfort Number: This is the monthly payment that won't keep you up at night - the one that lets you still save for retirement, take a vacation now and then, and not panic when your car needs unexpected repairs.

For most of my clients making $50k, their comfort number is about 10-15% lower than what lenders approve them for. That might mean a house that's $195,100 instead of $275,700.

How location affects affordability

Your $50k salary is going to stretch VERY differently depending on where you're house hunting. For example, here is a table with examples of what your salary might be able to afford you in each state across the United States. I also threw in average tax and insurance rates so you can compare.

State | What $50k per year gets you | Average Sales Price | Average Annual Taxes | Average Annual Insurance |

|---|---|---|---|---|

Alabama | An average home in good condition | $235,675 | $703 | $1,610 |

Alaska | An average home in good condition | $381,744 | $3,965 | $1,067 |

Arizona | Small starter homes that need some work | $435,839 | $1,692 | $917 |

Arkansas | An average home in good condition | $203,067 | $957 | $1,611 |

California | A mobile home or fixer upper if you're lucky | $776,000 | $4,579 | $1,403 |

Colorado | Small starter homes that need some work | $561,205 | $2,230 | $1,802 |

Connecticut | Small starter homes that need some work | $403,750 | $5,963 | $1,651 |

Delaware | Small starter homes that need some work | $399,857 | $905 | $988 |

Florida | Small starter homes that need some work | $405,289 | $3,154 | $2,437 |

Georgia | An average home in good condition | $333,903 | $2,499 | $1,466 |

Hawaii | A mobile home or fixer upper if you're lucky | $851,930 | $2,266 | $1,299 |

Idaho | Small starter homes that need some work | $456,839 | $1,873 | $884 |

Illinois | An average home in good condition | $286,413 | $4,575 | $1,223 |

Indiana | An average home in good condition | $238,411 | $1,690 | $1,058 |

Iowa | An average home in good condition | $203,770 | $2,573 | $1,043 |

Kansas | An average home in good condition | $238,824 | $2,235 | $1,491 |

Kentucky | An average home in good condition | $211,235 | $1,122 | $1,232 |

Louisiana | An average home in good condition | $190,900 | $960 | $2,259 |

Maine | An average home in good condition | $384,783 | $3,206 | $996 |

Maryland | Small starter homes that need some work | $436,985 | $3,368 | $1,238 |

Massachusetts | Small starter homes that need some work | $640,113 | $6,059 | $1,712 |

Michigan | An average home in good condition | $262,814 | $1,902 | $993 |

Minnesota | An average home in good condition | $348,126 | $3,223 | $1,607 |

Mississippi | An average home in good condition | $183,507 | $891 | $1,766 |

Missouri | An average home in good condition | $259,250 | $1,554 | $1,340 |

Montana | An average home in good condition | $388,053 | $2,634 | $1,471 |

Nebraska | An average home in good condition | $262,637 | $3,193 | $1,684 |

Nevada | Small starter homes that need some work | $445,883 | $1,803 | $863 |

New Hampshire | Small starter homes that need some work | $500,429 | $5,726 | $1,090 |

New Jersey | Small starter homes that need some work | $523,500 | $7,978 | $1,309 |

New Mexico | An average home in good condition | $301,000 | $1,045 | $1,229 |

New York | Small starter homes that need some work | $476,429 | $6,110 | $1,455 |

North Carolina | An average home in good condition | $340,330 | $1,617 | $1,192 |

North Dakota | An average home in good condition | $253,116 | $2,831 | $1,256 |

Ohio | An average home in good condition | $230,500 | $2,401 | $920 |

Oklahoma | An average home in good condition | $200,378 | $1,332 | $2,155 |

Oregon | Small starter homes that need some work | $511,434 | $3,768 | $793 |

Pennsylvania | An average home in good condition | $279,709 | $3,215 | $1,014 |

Rhode Island | Small starter homes that need some work | $487,985 | $4,837 | $1,900 |

South Carolina | An average home in good condition | $301,057 | $1,008 | $1,432 |

South Dakota | An average home in good condition | $318,000 | $2,219 | $1,270 |

Tennessee | An average home in good condition | $327,855 | $1,110 | $1,368 |

Texas | An average home in good condition | $314,750 | $4,141 | $2,146 |

Utah | Small starter homes that need some work | $530,041 | $2,517 | $831 |

Vermont | Small starter homes that need some work | $411,381 | $4,218 | $1,025 |

Virginia | Small starter homes that need some work | $394,678 | $2,658 | $1,199 |

Washington | Small starter homes that need some work | $609,540 | $4,242 | $1,001 |

West Virginia | An average home in good condition | $167,110 | $582 | $1,016 |

Wisconsin | An average home in good condition | $305,000 | $3,165 | $780 |

Wyoming | An average home in good condition | $344,432 | $1,612 | $1,432 |

See what I mean? The same $50k salary might make you house-poor in one city and practically rich in another! And don't forget that property taxes can dramatically impact your monthly payment.

This is why most 'how much house can I afford' calculators can be so misleading - they rarely account for these massive regional differences that can make or break your budget. Our calculator above automatically pulls in your exact location to give you a proper recommendation.

The takeaway? If you're flexible on location and working remotely, your $50,000 can go WAY further in some markets. I've had clients literally double their square footage by moving just one state over!

Steps to take

Alright, so you've crunched the numbers and you're feeling pretty good about your home buying power on that $50k salary. What now? Here's your game plan:

Step 1: Get pre-approved ASAP

This isn't the same as pre-qualification! Instead, a pre-approval means a lender has actually checked your credit, verified your income, and is ready to lend you a specific amount. In today's competitive market, sellers won't even look at offers without this. Plus, it gives you a crystal-clear budget to work with!

Step 2: Find a real estate agent who GETS your budget

Not all agents are created equal! Some will try to push you toward the top of your budget (hello, bigger commission), while others truly understand the importance of financial comfort. At Bellhaven, we specialize in finding that sweet spot – amazing homes that won't leave you eating ramen for dinner.

Step 3: Make your must-have list (and be brutally honest)

Granite countertops? Extra bathroom? Yard for the dog? What are your non-negotiables vs. your 'nice-to-haves'? Be real with yourself – and remember that you can always renovate later, but you can't change the location!

Step 4: Start touring homes in person

Online listings can be SUPER misleading. That 'cozy' bedroom might be the size of a closet, and that 'charming' kitchen might have a weird layout that drives you nuts. Get in there and feel the vibe!

Step 5: Run the REAL numbers on any contender

Before making an offer, calculate everything – mortgage, taxes, insurance, HOA, average utilities, commuting costs from that location, etc. Don't forget to factor in any immediate repairs or updates!

The coolest part? You don't have to figure all this out alone. That's literally what we're here for! At Bellhaven Real Estate, we've helped hundreds of folks making $50,000 find homes that hit their sweet spot of awesome without the financial stress.

Ready to turn those calculations into keys in your hand? Let's chat! A 15-minute call can save you months of frustration in your home search.